Posts from June 2021

Real Estate In Sunriver

RSS Feed

RSS Feed

RSS Feed

Central Oregon Employment | 2 Posts

Central Oregon Housing Market | 10 Posts

Central Oregon Lifestyle | 2 Posts

Cleaning Tips | 1 Posts

Finance | 1 Posts

First Time Homebuyers | 1 Posts

Golf | 1 Posts

Home Improvements | 3 Posts

Lifestyle | 2 Posts

Mortgages | 1 Posts

Moving Tips | 1 Posts

Real Estate Information | 1 Posts

Real Estate Market Updates | 2 Posts

Selling Your Home | 3 Posts

Sunriver Owners | 1 Posts

Sunriver Real Estate | 13 Posts

June

30

30

Debt-to-Income Calculation

Debt-to-Income Calculation

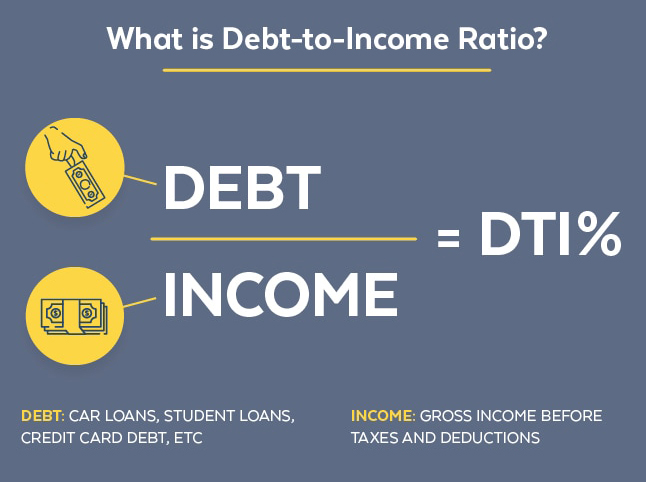

If you are considering purchasing a home soon, you need to be familiar with your debt-to-income calculation. Understanding this simple math formula could mean the difference between getting approved or getting denied for a home loan.

The discussion below will explain how to calculate this ratio and how it is used by mortgage lenders to approve people to buy a home.

The debt-to-income ratio, also called the DTI ratio by the mortgage industry, is a comparison between how much money people are making versus how much is being spent on debt.

The formula looks like this:

Total monthly debt payments ÷ monthly income = DTI

Here is a simple example that will explain how the math works.

Shawn and Linda have been married for 3 yea...